Earnings Reports, 5/6/2021 (2)

Earnings Reports, 5/6/2021 (2)

The last of this tidal wave of earnings reports.

Alright, it is finally time for my thoughts on the last of these earnings reports. Most of these companies reported on May 6, but a few reported afterward. These articles in my Earnings Reports series are usually behind a paywall, but I made this one available for free. If you like my analysis here and do not want to miss further articles, make sure you subscribe using the button below. There is also a button for a 30 day free trial that you can use if you haven’t made up your mind yet. We have some great stocks reporting soon, including Honda (HMC), so you really won’t want to miss out. As always, before we get started, I would like to remind you that this is not investment advice.

ING

Up first is ING Group (ING). My old intrinsic value for ING was $15 per share, although this was a conservative estimate because of how large ING’s shareholder equity fluctuations were. ING reported earnings of $0.31 per share on $5.67 billion in revenue. There were no analyst expectations that I could find, but the market liked this result and ING jumped up on the news. Of course, we really care about the shareholder equity. ING increased its book by a few hundred million dollars, much more than my linear prediction for it. Accordingly, my IV for it has jumped to $17 per share.

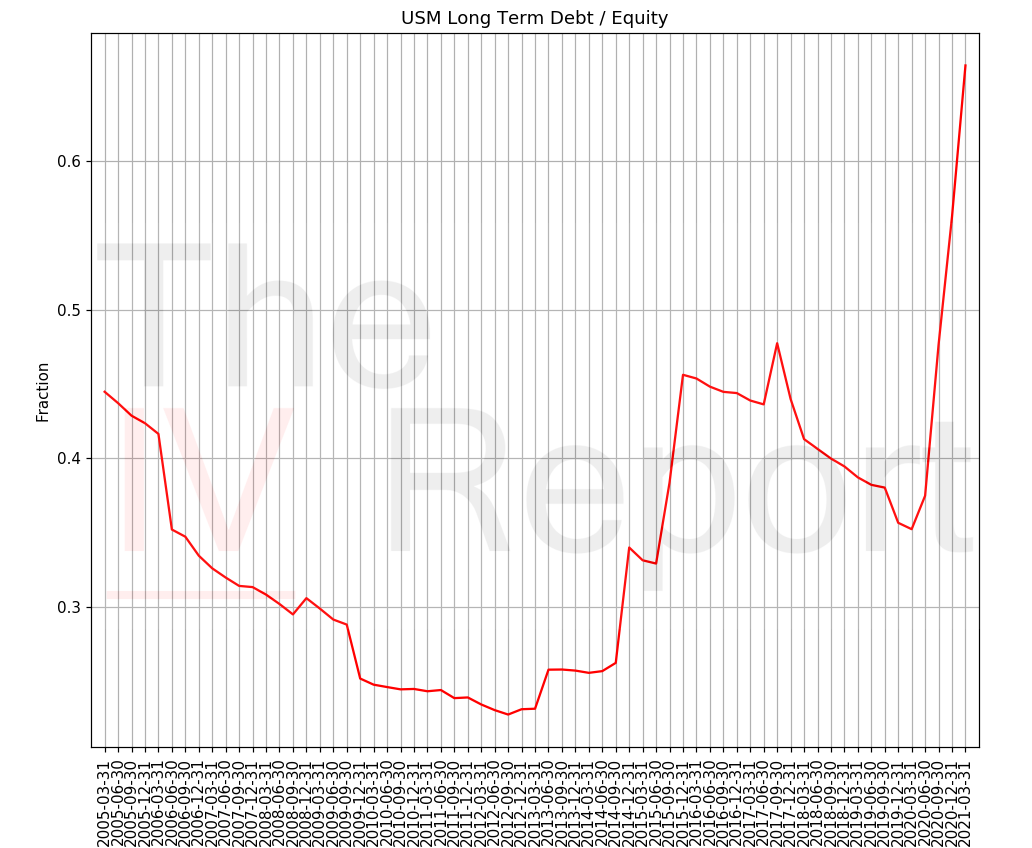

USM

United States Cellular (USM) is next. My previous IV for USM was $55 per share. USM reported EPS of $0.69 on revenue of $1.02 billion, beating expectations on both fronts. Shareholder equity was in line with my linear prediction. The most notable thing on this earnings report was the continuation of the recent spike in long-term debt, shown in Figure 1.

For now, USM’s debt situation is not too bad, but we will see how the situation develops. My IV for it remains $55 per share.

RGA

Reinsurance Group (RGA) is the first of a few disappointments that we are now going to go over. My previous price target for it was $240 per share. RGA reported a surprise loss of $1.24 per share on a revenue beat. Even worse, the book value per share went down by nearly $30! Correspondingly, my IV for RGA has decreased to $205 per share. I do think we will see RGA continue to climb into the upper $100s per share. I am currently up 20% on my position, and I would consider cutting my position before $205 if something else goes wrong.

BHF1

If you thought things were bad with RGA, the next two stocks will shock you. Brighthouse Financial (BHF) is not a good company, and I am not sure why I ever thought it was. For example, BHF lost $6.96 per share this quarter but “adjusted” it to show a $4.86 profit. I despise companies that hide behind these adjustments. Moreover, the company’s book value decreased by one third quarter-over-quarter. That is ridiculous. I immediately cut my position at $49.21 per share, locking in a 22% profit on the trade.

CNNE

Cannae Holdings (CNNE) is the next disappointment we will review. My previous IV for it was $55 per share. CNNE lost $2.55 per share on -$0.20 expected. That is a crazy miss, and it has left me down 7% on the trade. Moreover, its book value per share fell by about $6. Looking back, I am not really sure why I was so aggressive in valuing this company. The best I can do now on its IV is $42 per share, which is very close to my entry of $39.07. I am looking to exit the trade. If I get a profit (or close), I will almost certainly close. You can’t win them all, but I really should have just stayed out here and avoided the pain.

HOLI

We will end on some good news. Hollysys Automation (HOLI) missed on its EPS by 33%. Normally that would be a bad thing, but they still posted a $0.26 profit per share. Revenue was $110 million on $95 million expected. More importantly, HOLI increased its shareholder equity by $13 million, close to my linear model’s prediction. Thus, we have the perfect storm: HOLI increased its value, but has bad news. These setups are prime value investing buying opportunities. I have already bought more, and I plan on loading up on further dips. My previous IV was $22 per share, and I am keeping it the same.

That’s all for this article! The earnings reports are finally going to slow down for a bit, so I will be able to produce other content again (analysis-heavy articles like this take forever to write). If you enjoy my articles, you should consider joining my free mailing list or my paid subscription service ($5 per month or $50 per year). Don’t forget to share with your friends. See you again next time!

So none of the next three companies actually reported on May 6, but by pushing back this article I was able to include them here.